The Competition Authority has submitted a report on the draft bill to amend the Agricultural Produce Act. The Ministry of Food published the draft bill on the government's consultation portal on 10 November and invited the Competition Authority to submit a report on the same day.

The Competition Authority opposes the ideas set out in the draft bill from the Ministry of Food, which propose granting slaughterhouse operators a broad exemption from the basic principles of competition law.

The proposals in the draft bill are not designed to strengthen Icelandic agriculture. In the opinion of the Competition Authority, other and more effective ways must be sought to strengthen the position of Icelandic farmers and Icelandic agriculture, for the purpose of going on the offensive rather than on the defensive. The Competition Authority is ready to take part in such a discussion.

The Competition Authority has the task of taking action against anti-competitive practices by public authorities, advising the government on ways to promote competition, and drawing attention to laws and government regulations that run counter to the objectives of competition law. Part of this work is to provide government authorities with comments on draft bills or government regulations.

A copy of the Competition Authority's review can be accessed here,„Commentary on the draft bill on the consultation portal for the Act on amendments to the Agricultural Produce Act No. 99/1993 (restructuring of the slaughtering industry)“.

Below, the review is available by topic:

It is appropriate at the outset to summarise the main content of the draft bill and the underlying assumptions, with reference to the draft bill, the explanatory memorandum accompanying it, and the Ministry's responses to a query submitted by the Competition Authority.

This shall be further justified with reference to the draft bill, the ministry's responses and the Competition Authority's research in previous cases:

An insufficient assessment of whether the exemption rules of the current competition law apply

The provisions of Article 1 of the draft bill provide for the establishment and operation of a company jointly owned by the product processing plants. To make this possible, the draft bill provides for the company to be exempted from the prohibition on illegal collusion in Article 10 of the Competition Act and the prohibition on anti-competitive conduct by business associations in Article 12.

According to Article 15 of the current Competition Act, the establishment of an association of this kind is permitted if it contributes to improved production or distribution of a product, provides consumers (recipients of goods or services) with a fair share of the benefits arising from the association, does not impose unnecessary restrictions on participants in the cooperation, and does not enable them to prevent competition with regard to a substantial part of the products.

The draft bill indicates that the ministry's assessment is that the establishment of the company does not fulfil the aforementioned conditions of Article 15 of the Competition Act. Accordingly, the following is stated in the explanatory memorandum: „It has been considered that the relevant provision of Article 15 of the Competition Act does not provide sufficient scope for cooperation, in particular because it is not permitted to take the interests of producers into account, and therefore a specific authorisation for cooperation needs to be enacted in the Agricultural Produce Act.“

As the Competition Authority is not familiar with the aforementioned explanation of the explanatory memorandum to Article 15, the authority requested information on which interpretation the drafters were referring to, i.e. what assessment had been carried out that the exception in Article 15. Article could not cover the establishment of the company. Memos and other documents on this were requested. From the ministry's response, it can be inferred that it did not conduct its own assessment, but merely refers to submissions from interest groups. The ministry's response thus states the following: „This refers to joint submissions from stakeholders to the government.“. The reply was accompanied by the attached joint submissions of the Association of Business, the Federation of Industry and the Farmers' Association of Iceland, dated 12 November 2020, 7 December 2020 and 15 January 2021. The application of Article 15 will be discussed in more detail in Chapter 4 below.

Furthermore, the explanatory memorandum to the draft bill and the ministry's responses to the Competition Authority indicate that no assessment has taken place that is comparable to the assessment required to be carried out under Article 15 of the Competition Act.

The establishment of the association is permanent.

Article 2 of the draft bill proposes that the exemption from Articles 10 and 12 of the Competition Act will expire on 1 January 2026. Accordingly, the draft bill assumes that the establishment and operation of the association would be unlawful under Articles 10, 12 and 15 of the Competition Act in the absence of legislative changes. On this assumption, it must be considered that the association's activities would become unlawful again when the provisions of clause 1 of the draft bill cease to have effect.

For this reason, the Competition Authority requested that the ministry clarify its understanding of the legal effect of the time limit, including whether the ministry anticipated that the company's operations would cease when the authorisation expired. The ministry's response states that the company is expected to be able to operate indefinitely, „that its activities are within the competition law“.

From the ministry's response, no other conclusion can be drawn than that the legal effects of establishing a company on the basis of the exemption are intended to be permanent. It is therefore not, in practice, a temporary provision. The temporal limitation of the provision therefore appears to be intended solely to define the period available for processing plants to commence cooperation.

On the other hand, the ministry's response does not justify how the activities of an association established on this basis will become lawful upon the repeal of the provision, since it is assumed that an exemption from the law is a prerequisite for its establishment and operation until 1 January 2026.

An exemption applies to merger rules, at least in certain circumstances.

According to the draft bill, the exemptions from competition law for the establishment of a company are limited to the prohibitions in Articles 10 and 12 of the Competition Act, and the explanatory memorandum states that „Compliance with competition law otherwise applies in full“. However, these comments in the explanatory memorandum do not seem to hold up.

The reason is that the establishment of a jointly owned company by competitors, intended to take over specific, well-defined tasks on a permanent basis and to operate independently, can be considered a merger for the purposes of competition law (e.g. joint venture) Consequently, the Competition Authority asked the ministry whether the draft bill should be interpreted in such a way that the establishment of a company could fall within the scope of the Authority's merger control. The Ministry chose not to answer the question but stated that by publishing the draft bill on the consultation portal, it was seeking the views of stakeholders.

In light of the foregoing, no conclusion can be drawn from the draft bill other than that the intention is also to set aside the merger rules of competition law where they apply to the establishment of a company of this kind. The reason is that the exemption in the draft bill would, by its very nature, be rendered meaningless if the establishment of a company (e.g. joint venture) would, as is the case, fall within the remit of the Competition Authority on the basis of the merger provisions of the Competition Act. As is set out later in the opinion, the examination of mergers is largely aimed at assessing matters analogous to those considered when applying the exemptions in Article 15 to Articles 10 and 12.

The companies to which the exemption applies

It is of great significance in this matter that it is established which companies the draft bill's exemption is intended to apply to, and what effect the said exemption would have on market operations. In the explanatory memorandum to the Bill, 19 slaughterhouse operators are listed, and it is rightly noted that some of them are owned by other slaughterhouse operators and are therefore, by their very nature, not independent competitors. Furthermore, the list includes micro-slaughterhouses.

Consequently, the supervisory authority requested information from the ministry as to whether it had assessed and taken a position on which parties on the list are considered independent competitors, etc. which operators operate independently of other slaughterhouse operators and who receive or are likely to receive animals from farmers other than those they currently service. The ministry's response stated that it had not taken a position on this.

A review of the list of slaughterhouse operators in the explanatory memorandum to the draft bill, in light of previous investigations by the Competition Authority, shows that the independent competitors, excluding micro-slaughterhouses, that take sheep in the country are in practice four in number, i.e. KS, Norðlenska Kjarnafæði, SS and Fjallalamb. Other companies are owned by, or have significant ownership ties to, the three largest companies. There are also four independent competitors that take livestock, three of which are the same as those in sheep slaughter, namely KS, Norðlenska Kjarnafæði and SS, plus B Jensen in Akureyri. In addition, four take pigs and three take poultry.

Plans for a monopoly, or something close to it

In the ministry's response to the Competition Authority, it is stated that it is unclear what measures the meat processing plants will take under the authorisations. However, the memorandum accompanying the draft bill states that the assumptions underlying the existing analyses from Deloitte in 2021 are based on the number of sheep abattoirs being reduced to 3-4 and large-scale abattoirs becoming two. The Deloitte analysis, however, does not include pig or poultry slaughter.

However, considerable guidance on the plans of slaughterhouse operators can be found in the letter from the Federation of Icelandic Businesses, the Federation of Icelandic Industries and the Farmers' Association to the government of 12 November 2020. It states that the National Association of Slaughterhouse Operators considers it feasible to slaughter all the sheep in the country in two to three abattoirs. It is also considered sensible to reduce the number of abattoirs for cattle and horses to two in the country. From this, it must be concluded that the slaughterhouse operators are planning for up to one sheep slaughterhouse in North Iceland and one in South Iceland. There will also be one large-animal slaughterhouse in each of the two regions. It is likely that the said abattoirs will all be owned by a joint company, and the draft bill places no restrictions on this.

Various core elements were not assessed during the preparation of the bill.

The memorandum accompanying the draft bill states that if no action is taken that „the need for rationalisation and restructuring in the operation of meat processing plants is likely to increase, with unforeseen built and social impacts“. On this basis, the Competition Authority requested information on what assessment or data underpins this conclusion, such as memoranda or reports from the Icelandic Agency for Regional Affairs or other parties. Information was also requested on whether the ministry had assessed the regional and social impacts of the proposed legislative changes. The authority had, in particular, in mind the aforementioned plans by the National Association of Slaughterhouse Operators to reduce the number of abattoirs. In the ministry's responses, reference is made to a 2003 report on strategy for sheep slaughter and a summary from the Icelandic Rural Development Authority on the state of sheep farming from May 2022. In the view of the Competition Authority, the former report has limited relevance here, e.g. because much of the information contained in the report is outdated, and the latter report is an interesting discussion of the geographical distribution of sheep farmers, etc., but says nothing about the development effects of the reduction in the number of abattoirs.

It is clear from the memorandum accompanying the draft bill and the ministry's responses that, in preparing the bill, no quantitative data was obtained from slaughterhouse operators regarding potential rationalisation or how it should be achieved. Furthermore, it appears that the slaughterhouse operators have not been asked to account for why they have not each already undertaken further rationalisation through the reduction of abattoirs, as KS, SS and Norðlenska Kjarnafæði each operate more than one abattoir in a specific region.

In light of the above, no economic assessment has been carried out on the situation of meat processing plants or potential rationalisation, covering all the companies to which the draft bill applies. With regard to likely economic efficiency gains, the Ministry refers solely to Deloitte's 2021 analysis and other general reports and studies produced in recent years, but that discussion does not cover all the activities that would fall under the exemption. It is also worth noting that the Deloitte report states that „Marketers“ ideas about opportunities for optimisation in meat processing are poorly developed.“ and „Opportunities for manipulation at slaughter are in the current legal framework“(SE bolding).

This is discussed in more detail later in the review.

An analysis of the position of farmers in relation to meat processing plants has not been carried out.

Exemptions for processing plants in Norway and the EU are based primarily on the conditions that the companies in question are owned by farmers and that competition oversight is guaranteed. A key prerequisite for farmers to benefit from the consultation or merger of processing plants is that they can exercise ownership oversight, benefit from competition between processing plants, or, as a last resort, from public protection, for example with regard to pricing and access.

Consequently, the Competition Authority requested, among other things, documents and information from the ministry regarding the ownership of the aforementioned slaughterhouse licensees. In response, the ministry referred to the companies' annual accounts, which are available in the company register. It can be inferred from the response that no analysis of this was carried out during the preparation of the bill. Furthermore, the exemptions contained in the draft bill are not dependent on farmers being able to exercise ownership oversight to protect their interests. The exemptions therefore go much further in this respect than those in Norway and the European Union.

From the information available, it is clear that the slaughterhouse operators referred to above are to a negligible extent owned or controlled by farmers. Furthermore, previous investigations by the Competition Authority have revealed that farmers themselves consider their negotiating position vis-à-vis processing plants to be poor. This will be discussed in more detail later in the opinion.

Definition of the exemption and conditions inadequate

According to the draft bill, the exemption in question is clearly limited to the activities of a company which is only permitted to carry on specific business. The activity would be subject to conditions intended to protect the interests of farmers and promote competition. Upon closer inspection, it is clear that the scope of the exemption is not clearly defined. Furthermore, the implementation of the derogation and the likely development of the competitive environment for meat processing plants mean that the conditions stipulated will have limited significance. This is further justified in section 10 below.

When competition is eliminated and farmers, other businesses and consumers are unable to hold processing plants to account, the government has little choice but to protect the interests of these parties through public regulation, such as by means of public pricing. This is not addressed in the draft bill.

No assessment has been made as to whether the provisions of the draft bill are contrary to the EEA Agreement.

Finally, it should be noted that from the draft bill and the ministry's responses, it is clear that it has not been established that the aforementioned legislative amendment is consistent with the EEA Agreement. As such, the proposals in the draft bill may constitute a breach of international obligations. This will be discussed later in the opinion.

The ministry has also stated that no competition assessment has been carried out on the draft bill beyond what is set out in the form available on the consultation portal.

The draft bill contains a list of 19 slaughterhouse operators, but the market's activities are not described further. Based on information from the Competition Authority's public data and a previous review, the current market position of the main players and their activities can be described as follows.

i. Definition of markets

In decision no. 12/2021, Merger of Norðlenska, Kjarnafæða and SAH Afurða, the relevant product markets in the case were considered to be as follows:

The geographical markets for slaughter were considered to be divided into two markets, namely the Northern and the Southern regions. The proximity to a slaughterhouse was considered a dominant factor in the farmers' choice. Furthermore, regulations on slaughter and the transport of livestock, as well as considerations of animal welfare and product quality, have a limiting effect on the distance it is practical to transport live animals for slaughter.

Last but not least, the Competition Authority's analysis indicated that the additional cost of transporting livestock is considerable as a proportion of the product price, and even greater when compared to the cost of slaughter. The analysis thus suggested that when the transport distance for sheep and cattle reaches 100-200 km, transport costs can be expected to amount to around 5-10% of the product price. This increases, as is to be expected, with longer distances.

The geographical market for processing and wholesale, however, was considered to be the entire country.

ii. Slaughter, by type

In the North, the largest players are Kjarnafæði Norðlenska (KN) and KS and affiliated companies, with an 85-90% share of the sheep slaughter market in 2019. The same companies had a 70-75% share of the beef slaughter market in the same region. KN then had a 60-65% share of the pig slaughter market in North Iceland.

In the South of Iceland, SS had a [95-100]% share of sheep slaughter in 2019. In cattle slaughter, SS has a [50-55]% share and KS (Hellu Abattoir) has a [45-50]% share. Stjörnugrís also operates a pig slaughterhouse with a [90-95]% share in 2019, and Ísfugl and Matfugl operate poultry slaughterhouses.

The three major slaughter licence holders operate several abattoirs and are linked to others through minority ownership. Thus, KN slaughters sheep in Húsavík and Blönduós and cattle in Akureyri and Blönduós in its own abattoirs. KN also owns a one-third stake in Sláturfélag Vopnfirðinga. KS slaughters sheep in Sauðárkrókur, and cattle in Sauðárkrókur and Hella. KS also owns a 50% stake in the KVH Slaughterhouse, which operates in Hvammstangi. SS runs one sheep slaughterhouse, one cattle slaughterhouse and one poultry slaughterhouse.

iii. Processing and wholesale of fresh meat on the one hand, and processing and wholesale of processed meat on the other.

In the fresh lamb processing and wholesale market in 2019, KN had a [45-50]% share, KS and associated companies had [15-20]% share and Fresh Meat Products followed with a [10-15]% share. In the processed lamb meat processing and wholesale market in 2019, KN held a [45-50]% share. SS had the second-highest share, [30-35]%, and KS and associated companies had a [5-10]% share.

In the market for the processing and wholesale of fresh beef in 2019, KN held a [35-40]% share, KS and associated companies [15-20]%, and Fresh Meat Products [15-20]%. In the processed beef processing and wholesale market, SS had the highest share, at [50-55]%, KN with [20-25]%, and KS and related companies with [10-15]%.

In the market for the processing and wholesale of fresh pork in 2019, Stjörnugrís had a [45-50]% share, Síld og fiskur [20-25]% and KN [15-20]%. In the processed pork processing and wholesale market, Silverside and Fish had the highest share, at [30-35]%, followed by KN with [25-30]% and SS with [15-20]%.

In the market for the processing and wholesale of fresh horse meat in 2019, KN was the largest with [40-45]%. SS had a [25-30]% share and KS and related companies had [20-25]%. In the processed and wholesale market for horsemeat in 2019, SS had the highest share, at [50-55]%, KN the second largest, at [35-40]%, and KS and its affiliated companies followed with [5-10]%.

As the above discussion shows, meat processing plants are among the largest players in the markets for the processing and wholesale of fresh and processed meat. The only company that does not slaughter animals and is among the largest firms is Ferskar kjötvörur, owned by Haga.

The memorandum accompanying the draft bill states that the aim of the proposals to exempt product processing plants from the general rules of competition law is to „to support the restructuring and rationalisation of slaughtering and meat processing. The legislation also proposes that the objectives of the Agricultural Produce Act be pursued, namely to promote progress and increased efficiency in the production, processing and sale of agricultural produce. to the benefit of producers and consumers“ (SE emphasis).

The stated objective of the draft bill is, in other words, to achieve an efficiency gain for the benefit of producers and consumers. Contrary to what might be inferred from the draft bill, however, the objectives of the measures are well aligned with those of the current competition law. Given the stated objectives of the draft bill, there is therefore no need to set competition law aside; on the contrary, it can facilitate efficiency gains, whilst at the same time protecting the interests of farmers, other customers of produce processing facilities, and consumers. This shall be further justified.

It is undisputed that effective competition leads to greater operational efficiency, less waste and better corporate governance. Competition also promotes innovation and progress in business, a wider range of products, better services and better prices for customers. Furthermore, recent research suggests that active competition is one of the factors that can contribute to increased food security. The effects of competition are discussed in more detail in Report of the Competition Authority No. 1/2021.

The interpretation and application of the prohibition on unlawful cooperation in Article 10 of the Competition Act and Article 12 concerning restrictive practices by associations of undertakings takes particular account of considerations of business efficiency, cf. the provisions of Article 15 of the Competition Act. The same applies to the interpretation and application of the merger rules of Articles 17 to 17(e) of the Competition Act.

It is appropriate to elaborate further on how competition law facilitates this kind of optimisation, without sacrificing the aforementioned benefits of competition.

4.1. The application of Article 15 of the Competition Act is well-suited to the interests of farmers and consumers

Provision 15 of the Competition Act permits companies to cooperate, including to achieve economies of scale and reduce operating costs, provided that certain specified conditions are met. These conditions are primarily concerned with ensuring that the operational benefits of collaboration are not solely for the benefit of the collaborating companies and their owners, but that customers also receive a fair share of the benefits. This is done, for example, by ensuring that competitive constraints remain in place.

The substantive provision of Article 15 reads as follows:

„A prohibition under Articles 10 and 12 shall not apply if agreements, decisions, concerted practices or decisions of undertakings or associations of undertakings:

Paragraph a refers to the economic objective that the cooperation is intended to achieve. Operational optimisation, better utilisation of production facilities, improved collection and distribution, etc., are all matters covered by paragraph a. Paragraph b requires that consumers enjoy a fair share of the benefits arising from the cooperation. Such benefits may, for example, take the form of better terms or the quality of goods and services. In this context, 'consumers' refers not only to consumers in the narrow sense but also to other customers of the partner companies, such as suppliers in the case of a co-operation between processing plants.

Paragraph c requires that the cooperation does not impose on the undertakings restrictions which are not necessary for the achievement of the objectives. In this context, for example, reference could be made to the fact that the cooperation does not include more elements than are necessary for the objectives to be achieved. Under d), it is required that the collaboration does not enable the undertakings to prevent competition with regard to a substantial part of the relevant production or services. In the case at hand, it is, for example, crucial that producers' access to raw materials is not unduly restricted, and that the commercial interests of farmers regarding the choice of a produce-processing facility are not jeopardised.

The draft bill appears to be based on the assumption that it is not possible to pursue the interests of farmers under section 15 of the Competition Act. The explanatory memorandum states the following in this regard: „It has been considered that the relevant provision of Article 15 of the Competition Act does not provide sufficient scope for cooperation, in particular because it is not permitted to take the interests of producers into account, and therefore a specific authorisation for cooperation needs to be enacted in the Agricultural Produce Act.“

In the opinion of the Competition Authority, the above conclusion cannot be substantiated. It is explicitly provided that better utilisation of production facilities, improved collection and distribution can justify an exception to the prohibition on cooperation between undertakings. It is also recognised in European competition law that the condition of ensuring that consumers receive a share of the benefits of the cooperation also includes other customers of the cooperating undertakings, such as farmers (suppliers), as discussed above.

In its query to the ministry, the supervisory authority requested further clarification on the interpretation set out in the explanatory memorandum. In the ministry's responses, no independent reasoning was provided, but instead reference was made to a joint submission from the Confederation of Icelandic Enterprise, the Federation of Icelandic Industries and the Farmers' Association of Iceland, dated 12 November 2020, 7 December 2020 and 15 January 2021.

This is discussed in the aforementioned letter from the interest group to the government, dated 15 January 2021. It cites a memorandum from Logos, which was apparently prepared for the interest group, stating that the experience of many people in the business community is that „The Competition Authority interprets its powers very broadly and the scope for business activity very narrowly.“

This statement is not further substantiated and is not supported by any evidence. Until 1 January 2021, the Competition Authority was responsible for granting exemptions under Article 15 of the Competition Act. Of the applications on which decisions were made, a waiver was granted in the vast majority of cases, in some instances without conditions, but in many cases with conditions aimed primarily at better defining the cooperation and ensuring that customers and consumers would benefit from it. In interpreting the substantive provisions of Article 15, the Competition Authority has consistently taken into account case law and interpretations in EEA/EU law. The aforementioned assertion in the interest group's letter to the government is therefore unfounded.

From 1 January 2021, the implementation of Article 15 was changed in such a way that, instead of the Competition Authority granting an exemption from the prohibition on collusion, companies are tasked with so-called self-assessment. This change was made by Act no. 103/2020, amending the Competition Act. The change was made, not least, on the recommendation of business interest groups. Following the change, or in December 2020, the Competition Authority established specific Guidelines on the application of Article 15...which aims to facilitate the aforementioned self-assessment for companies.

In the aforementioned letter from the interest group to the government, reference is made to the aforementioned Logos memorandum, which states that it entailed „a significant legal risk for the processing plants and their staff to take that route [to work together on the basis of Article 15] Clearly, it is not possible to undertake the necessary actions and investments with such a risk hanging over us. We therefore do not consider this option to be viable.“

These arguments cannot be accepted. As set out above, the legislature entrusted companies with self-assessment when applying the exemption rules of Article 15. clause. It can in no way be argued that there is a greater risk for meat processing plants in the meat industry in applying this self-assessment than for companies in other markets. Should the authorities accept arguments of this kind, it would necessitate a review or revocation of the self-assessment introduced by Act No. 103/2020, which must apply to all companies.

In light of the foregoing, it has not been justified whether and, if so, which of the conditions for the derogations in Article 15 from the prohibition on cooperation is responsible for the failure to achieve optimisation in the slaughter industry.

To date, the application of Article 15 has not been tested with regard to cooperation between meat processing plants. The reason is that during the period when the Competition Authority was authorised to grant exemptions under Article 15 of the Competition Act, meat processing plants never submitted a request for an exemption to the Authority for the type of cooperation envisaged in the draft bill. However, they were repeatedly advised of this option, both by the Competition Authority and the Ministry.

However, it should be noted that in June 2017, the Lamb Meat Marketing Board submitted an exemption request to the Competition Authority on the basis of Article 15 of the Competition Act. The request concerned, in particular, cooperation on the export of lamb meat which involved each slaughterhouse operator committing to export a specified proportion of the lamb meat they produced, or approximately 351 tonnes. The plans therefore involved the management of supply in the domestic market.

The Competition Authority examined the request and sought, among other things, submissions from interested parties. However, it was not possible to make a final decision on the request as the Marketing Board did not comply with the Competition Authority's request for the data on which the request was based. The Council did not comply with the Authority's request to provide preparatory documents, nor did it respond to a request to confirm whether such documents existed. Consequently, the Authority considered it unavoidable to provide a preliminary assessment based on the limited information available. The supervisory authority could draw no other conclusion than that the council's preparation of the case was seriously deficient. However, this was not a final decision, and the Marketing Council made no further pursuit of the matter.

In light of recent events, the Competition Authority published News on the matter on its website on 3 August 2017. There, the supervisor's letter to the Marketing Board, dated 1 August 2017, is made available.

From the above, it is clear that there is nothing to prevent the provisions of Article 15 on exemptions for cooperation between undertakings from creating a basis for optimisation in the meat processing sector, provided that the arguments and interests of farmers, other customers and consumers are secured. Exempting meat processing plants from the obligations of Article 15 has the sole purpose of granting them an exemption from the protection that the provision affords to farmers, other customers and consumers.

The intended optimisation of meat processing plants is discussed in more detail in Chapter 9 below.

4.2. Competition law merger rules have been applied to facilitate rationalisation while at the same time protecting the interests of farmers, independent processors and consumers

As set out in Chapter 2, it follows from the draft bill that it is in effect intended to set aside the merger rules of competition law as well. The reason is that the establishment of a joint venture by competitors, intended to take over certain specific, well-defined tasks on a permanent basis and to operate independently, constitutes a concentration within the meaning of competition law (e.g. joint venture). From the ministry's answers to the Competition Authority's inquiry, the joint venture of meat processing plants is intended to operate permanently, despite the authorisation clause in the draft bill being intended to be of short duration. The draft bill's exemption would, by its very nature, be rendered moot if the establishment of a company (e.g. joint venture) would otherwise fall to the Competition Authority on the basis of the merger provisions of the Competition Act.

Articles 17 to 17e of the Competition Act provide for the supervision of mergers in Iceland by the Competition Authority. Under section 17c of the Competition Act, the Authority must intervene in mergers that either create or strengthen a dominant position, or otherwise significantly distort competition.

When assessing the legality of mergers, account shall also be taken of technological and economic progress, provided that it benefits consumers and does not impede competition. The Competition Authority must therefore take into account arguments and viewpoints regarding the efficiencies that may result from the merger. As with the assessment of the 15th article's exemption provisions, consideration is given, among other things, to whether the merged undertaking will continue to face constraints and whether the efficiencies resulting from the merger will deliver benefits for customers and consumers.

The issue of meat processing plants was recently under consideration in connection with the merger of Norðlenska, Kjarnafæður and SAH. The merger was established due to the companies' difficult operating situation, and it was argued that it would create opportunities for operational efficiencies, which would give the merged company the opportunity to better serve its customers and pay farmers a better price for slaughtered animals.

Following a thorough investigation, the Competition Authority approved the merger. Decision no. 12/2021. During its investigation of the merger, the Competition Authority defined the relevant markets for the case, both product and geographical markets, and assessed the position of the merging parties in the market. The Competition Authority then investigated the competitive effects of the merger and took a position on the merging parties' arguments regarding the potential efficiencies that could result from it.

The Competition Authority's observations were directed not least at the position of farmers following the merger. The Authority considered, among other things, that as a result of the merger, farmers would not have full ownership of the combined enterprise. The authority sought, among other things, to ensure that farmers would enjoy the benefits of any potential efficiencies resulting from the merger. During its investigation, the Competition Authority conducted two surveys of farmers' opinions, thereby taking their views into account when making its decision in the case. The results of the surveys are detailed below.

The Competition Authority then took a position on the position of competitors and customers among processors, as well as the interests of consumers. The Competition Authority sought the views of stakeholders and, among other things, commissioned a consumer survey, which was taken into account when assessing the merger.

The Competition Authority concluded that the merger should be authorised, despite it involving a significant degree of concentration. In this regard, the operational position of the merged companies and plans for rationalisation were taken into account. However, the authority considered it necessary to impose conditions on the merger in order to protect the interests of farmers, other customers and consumers. The conditions were aimed, inter alia, at the following:

It has been a short time since this merger took place. Therefore, there is no experience yet of the progress of the synergies or of the conditions set for the merger. However, the most recent consolidated financial statements state that the management of the combined company believes the merger will contribute to significant operational synergies. They believe that the merger, cost-saving measures, access to credit lines and a planned refinancing will ensure the Group's going concern for the foreseeable future. The operation of the processing plants will be discussed in more detail below.

From the above, it is clear that the merger rules of competition law can facilitate rationalisation, whilst at the same time protecting the interests of farmers, independent processors and consumers. The Competition Authority has applied the provisions of the Competition Act with this in mind, as have sister authorities in neighbouring countries, see further chapter 5 below.

Exempting meat processing plants from merger control in any way therefore has the sole purpose of granting them an exemption from the protection that the rules provide for farmers, other customers and consumers.

The intended optimisation of meat processing plants is discussed in more detail in Chapter 9 below.

In the arguments of those who advocate for the exemptions proposed in the draft bill, it is often cited that domestic production facilities should be granted comparable exemptions from competition law, as is customary in Norway and within the European Union (EU).

It is worth emphasising in this context that the rules on this matter in Norway and within the EU are primarily aimed at, on the one hand, allowing farmers or companies owned by them to cooperate, not least to protect their interests vis-à-vis their counterparts, including independent produce processing plants. The exemptions therefore do not apply to processing plants that are not owned by farmers.

However, the rules are intended to maintain competitive discipline in the relevant activity as before. Thus, for example, it is not a consideration to permit a market monopoly on the basis of the rules.

The rules do not, however, cover company mergers. Merger control is therefore applied in Norway and within the EU to protect competition in the market and safeguard the interests of farmers, processing companies and consumers.

The proposals set out in the draft bills therefore go further than the exemptions in neighbouring countries, in at least three respects:

In a previous discussion on the comparison of regulation in this country with that in Norway and the EU, the Competition Authority has emphasised its position that it could well be considered to transpose into Icelandic law exemptions from competition law based on the same fundamental principles as those outlined above. As previously noted, however, such exemptions are of a different nature to those proposed in the draft bill.

The following is discussed in more detail in the appendix to this opinion:

In light of the foregoing, it is beyond doubt that proposals for exemptions comparable to those contained in the draft bill would not stand a chance of success in our neighbouring countries.

From the draft bill and the ministry's responses, it appears that it was not ensured that the aforementioned legislative amendment is in accordance with the EEA Agreement. The memorandum accompanying the draft bill states specifically: „The EEA Agreement does not fundamentally cover agriculture […] The Ministry therefore considers that the content of the Bill does not give rise to an assessment of its compatibility with […] Iceland's international obligations.“

For this reason, the Competition Authority turned to the EFTA Surveillance Authority (ESA) and requested information on the Authority's interpretation of the EEA Agreement in this regard.

An ESA memorandum on the case refers to the fact that, according to Article 8(3) of the EEA Agreement, the provisions of the Agreement shall only cover; a. products falling within chapters 25 to 97 of the Combined Nomenclature of Description and Statistics, with the exception of those products listed in Annex 2; and b. the products specified in Annex 3 in accordance with the special procedure set out therein.

Thus, the scope of the EEA Agreement is described with regard to specific categories of products, but this indicates that certain products fall outside the scope of the EEA Agreement, unless otherwise stated.

It is then stated that there is a two-stage process to determine whether a product falls within the scope of the EEA Agreement. Firstly, it must be established under which chapter of the Harmonised Description and Coding of Goods and Services („the list“) the relevant product falls. Secondly, it must be checked whether a product falling under chapters 25-97 is excluded pursuant to Annex II to the EEA Agreement, or whether a product falling under chapters 1-24 is included pursuant to Annex III to the EEA Agreement.

It is argued that meat and offal fall under Chapter 2 of the list, and therefore the provisions of the EEA Agreement generally do not apply to such products. However, this general principle is not without exceptions, and it should be borne in mind that only certain agricultural products are excluded from the provisions of the EEA Agreement, and not agriculture as such. Thus, for example, the agreement's health and food regulations apply to the processing and marketing of meat and offal.

It is noted that no sector is entirely excluded from the scope of the EEA Agreement, only certain products are. Furthermore, numerous provisions of the Agreement apply to products that would otherwise be excluded from its product scope. For example, Article 21 of the EEA Agreement on cooperation in customs matters and the facilitation of trade provides that „Notwithstanding paragraph 3 of Article 8, this Article shall apply to all products.“ Furthermore, Article 23 of the EEA Agreement provides that the areas of the Agreement referred to in that provision „shall apply to all products, unless otherwise stated.“ Furthermore, Article 65(1) on public procurement and Article 65(2) on intellectual property „apply to all products and services unless otherwise stated.“

ESA gives the example that the scope of the agreement is often a matter of contention when it comes to competition rules related to state aid. If state aid is „inseparably linked“ to trade in products falling outside the scope of the EEA Agreement pursuant to paragraph a or b of Article 8(3), the aid falls outside the scope of the EEA Agreement. However, if state aid concerns products that fall both outside and inside the scope of the EEA Agreement, such state aid must be notified in its entirety to the ESA. The ESA will then assess the extent to which the EEA rules apply to the state aid.

In this regard, ESA refers to Synnøve Finden the case concerned a payment scheme which subsidised the transport of liquid dairy products. Liquid dairy products fall under Chapter 4 of the list and are therefore, in accordance with Article 8 of the EEA Agreement, excluded from the scope of the EEA Agreement. However, the category of liquid dairy products covered by the payment scheme also included flavoured yoghurts, which are listed in Annex 3 to the EEA Agreement and therefore fell within the scope of the EEA Agreement. Therefore, the state aid was subject to the EEA rules, insofar as it related to products within the scope of the EEA Agreement. This ultimately led to a decision requiring the state aid to be recovered from the Norwegian State.

The ESA also refers to the case of Ferskir Kjötvörur. That case concerned the conditions of Icelandic law regarding the importation of raw meat. The Icelandic authorities had argued that the EU's agricultural system fell outside the scope of the EEA Agreement. The EFTA Court had confirmed that raw beef fell outside the scope of the agreement unless otherwise provided for in the agreement. However, the court ruled that „the scope of the EEA Agreement, as defined in Article 8 thereof, does not leave an EEA State free to lay down rules […] and is bound by the relevant provisions incorporated into the Annexes to the EEA Agreement.“

The judgment in the Fresh Meat Products case demonstrates that the restrictions of Article 8 of the EEA Agreement do not override the arrangements otherwise provided for by the EEA Agreement, either expressly in other provisions, protocols to the EEA Agreement, or by arrangements incorporated into any of the annexes to the EEA Agreement.

The ESA therefore considers it incorrect to assert that the content of the bill does not provide grounds for assessing their compatibility with Iceland's international obligations on the basis that agriculture is generally exempt from the application of the EEA Agreement.

Thus, agriculture as such is not exempt from the provisions of the EEA Agreement, but only certain agricultural products. And even though Article 53 of the EEA Agreement on anti-competitive agreements or concerted practices does not apply to certain agricultural products, specific goods and/or services related to agriculture may fall within the scope of the EEA Agreement. This is made clear in the aforementioned Synnøve Finden-case where state aid for the transport of liquid dairy products, i.e. agricultural products, nevertheless fell partly within the scope of the EEA Agreement. Furthermore, the various provisions of the EEA Agreement apply to Icelandic agriculture, such as health rules and rules on the handling of slaughtered produce, and they even apply to the handling of product categories that fall outside the scope of the Agreement pursuant to paragraph 3 of Article 8.

It is therefore ESA's position that a planned derogation from the application of Article 10. and 12 of the Competition Act could give rise to issues under Article 53 of the EEA Agreement, to the extent that the cooperation under the proposed exemption relates to goods and/or services covered by the EEA Agreement.

The Competition Authority hereby notifies the above. The Competition Authority also considers it appropriate to point out that the effects on trade between Member States (e.g. Effect on trade), which is referred to in the draft bills, needs to be considered on a case-by-case basis. As the market share of the parties concerned is high (even 100%) and their activities cover the entire country, it must be considered more likely than not that the conditions for the application of Articles 53 and 54 of the EEA Agreement would be deemed to be met. It should also be noted here that the production facilities export a portion of the products they manufacture, and it can therefore be assumed that the derogation may affect trade between Member States.

As previously stated, no specific analysis was carried out within the ministry on which products and services would fall under the derogation, but it follows from the above discussion that it would be necessary to set this out in detail when preparing a potential bill. It is therefore still unclear whether all the products fall outside the scope of the EEA Agreement.

Should the preparation of a bill on derogations from the core rules of competition law proceed, the Authority considers it inevitable that a detailed assessment will be carried out to determine whether the plans are compatible with the EEA Agreement. Otherwise, the Icelandic state may be found to be in serious breach of the Agreement.

The draft bill is based on the assumption that the interests of produce processors and their owners are entirely aligned with the interests of farmers. The same point has also been emphasised by those who advocate for the kind of exemptions proposed in the draft.

It is therefore assumed that the efficiencies resulting from the cooperation of meat processing plants will automatically lead to farmers receiving a higher price for their produce. This will also create scope for greater innovation and investment, to the benefit of farmers.

This discussion overlooks the fact that the priorities and interests of processing plants and farmers do not, by their very nature, align in all cases, particularly when processing plants are not entirely owned and controlled by farmers or where there is no competitive oversight. As an example, several likely priorities of a farmer on the one hand, and a meat processing plant on the other, can be set out in the following table:

| Likely farmer's priorities | Likely product plant priorities |

|

· Get the highest price for produce · Know in good time what price he is offered · Have the option to look elsewhere and thus create a check and balance · There is no need to transport animals long distances to the slaughterhouse, with the associated risks (animal welfare, product quality). · Influence how products are processed and have access to a wide range of product processing. · Have access to a varying level of service, e.g. processing products for their own use · Be able to create their own priorities, e.g. concerning organic farming, climate issues or traceability · Create direct relationships with consumers, restaurants and other clients · Ensure innovation · Create a solid foundation for one's own business, independent of others |

· An increase in the price of products has a negative impact on operations. · That owners receive a dividend from their share, regardless of whether they are farmers or not. · Ensure maximum economies of scale with high-throughput production lines and simple processing. · Protect previous investment, which can, for example, be expressed in the terms of trade, binding farmers to trade, etc. · Minimise operational uncertainty, e.g. by binding farmers into contracts and increasing cooperation with competitors. · Generate income from other operations and broaden the range of services, e.g. by bundling with other inputs for farmers. · Protect their market position. · Be able to respond to changes in the market, if necessary, e.g. due to competitive pressure · That managers and staff receive adequate pay. |

It is clear that the interests and priorities of farmers and meat processing plants can in many ways be aligned. The core of the matter, however, is that if farmers can create pressure on processing plants as owners, or competitive pressure as customers (e.g. the threat of looking elsewhere), the chances of farmers' and processing plants' interests aligning increase.

However, if there is no owner oversight or competitive pressure, a rift can develop between friends. A company in a monopolistic position, for example, has far less incentive to treat its customers well, ensure effective cost control in its operations, or pursue innovation compared to a company operating in a genuinely competitive environment. There is no reason to suppose that different laws apply in this respect to the operation of meat processing plants than to other businesses.

Ownership of processing plants is therefore of great importance. It is also useful to draw lessons from existing survey results on farmers' attitudes towards competition and their bargaining position. This should be examined in more detail below.

6.1. Meat processing plants are not owned by farmers except in part

As set out above, the ownership of processing plants is a significant factor when deciding whether to grant them exemptions from competition law. Thus, the exemptions for cooperation between processing plants in Norway and the EU are primarily limited to companies owned by farmers (producer organisations), see chapter 5 above and the appendix. In a response to an inquiry from the Competition Authority regarding the draft bill, it was stated that the ministry had not specifically considered the ownership of processing plants when preparing the bill.

Ownership of meat processing plants was examined in connection with the Competition Authority's investigation into the merger of Norðlenska, Kjarnafæði and SAH, see decision no. 12/2021. The competition authority thus gathered information on the ownership of the main processing plants, inter alia to shed light on the independence of, and relationships between, competitors in the market. It should be noted that circumstances may have changed to some extent since that time. It should also be noted that the findings have not been submitted to the processing plants or their owners.

Taken together, the information from the Competition Authority suggests that of the 7 slaughterhouse operators that take in sheep or cattle (which are not considered small or micro-slaughterhouses according to a list in the explanatory memorandum to the draft bill) farmers do not hold a clear majority ownership in any slaughterer. However, farmers hold the voting power at the general meetings of one slaughterhouse (SS) and enjoy a degree of minority protection in another (KN). Voting rights are then unclear in two further smaller slaughterhouse operators. The slaughterhouse operators that exclusively handle pigs or poultry, i.e. Stjörnugrís and Ísfugl, are owned by the producers, who also hold the voting rights in those companies. The company Matfugl is owned by Langasjávar ehf., which is the parent company of certain businesses in the production and distribution of food.

Exemptions in Norway or the EC would therefore not be available for optimisation or cooperation in Iceland, nor do they permit the creation of a monopoly position.

Kaupfélag Skagfirðinga

Kaupfélag Skagfirðinga (KS) operates the KS Meat Processing Plant and fully owns the Hellu Slaughterhouse, as well as holding a 50% stake in the Slaughterhouse of Kaupfélag Vestur Húnvetninga.

According to information provided by KS to the Competition Authority during the investigation of the merger case, there were 1,502 members as of 31 December 2020. When asked about the proportion of farmers to the total number of members, KS stated that it was certain that farmers made up around 10% of the membership, but around 16% in terms of subscribed capital. KS noted, however, that classification in this way did not reflect the number of farmers who were members of KS. Reasons for this could include the fact that where several people farm on a single holding, there is only one contributor. A contributor could also be a limited company established for the farming business, in which case no contributor connected to the farm would be on KS's list of members. Other factors could lead to the classification not reflecting the member's actual work, such as where the contributor is an employee of another.

For this reason, the Competition Authority conducted its own analysis of which of these 1,502 members could be considered farmers, but the definition used is much broader than the one generally applied when referring to farmers, such as the definition in ISTARF95. The above-mentioned broader approach was used to ensure that the farmers' ownership and influence in KS were not underestimated in this analysis. However, the effect of this methodology is that the influence and share of farmers in KS is likely overestimated, but this does not appear to affect the main conclusion regarding ownership and voting power. Firstly, all contributors, as well as all residents of the same farmstead, regardless of whether or not these individuals were engaged in any farming, were defined as farmers. Secondly, all members of KS who lived on farms where an individual on that farm was registered as a livestock owner in 2019 were defined as farmers, according to information from the Ministry of Fisheries, Agriculture and Innovation.

Based on the above-mentioned assumptions, however, the Competition Authority's initial assessment was that at most 26% of KS's members could be considered farmers at the time the investigation was based on, whether measured by the number of members or by share capital. Looking at the association's divisions, of which there are twelve (excluding the out-of-district division), farmers, according to the above analysis, were in the minority in 6 divisions, in one division half of the members, and in five divisions the majority of members.

In the opinion of the Competition Authority, the above indicates that Kaupfélag Skagfirðinga, and by extension the KS Meat Processing Plant and the Hella Slaughterhouse, are minority-owned by farmers. The fact that the cooperative is minority-owned by farmers means that any potential distributions from the cooperative go, in part, to the farmers. Furthermore, this indicates that farmers do not hold the majority of the voting power.

Slaughterhouse Society of Southern Iceland

The homepage of SS states that the company is a co-operative owned by agricultural producers in its area of operation and by general shareholders. The association's area of operation is West Skaftafell County, East Skaftafell County as far as the Jökulsá river on the Breiðamerkursand, Rangárvallasýsla, Árnessýsla, Kjós and Gullbringusýslur, Borgarfjörður, Mýrar, Snæfellsjökull and Hnappadalur, and Dalasýsla, as well as towns and settlements within the aforementioned areas.

The company owns Reykjagarður and Hollt og Gott in its entirety. Reykjagarður produces and sells poultry products under the Holta brand, and Hollt og Gott produces and sells salads and vegetables in consumer packaging.

The company's share capital is divided into so-called Class A and Class B shares. Only members of the company are eligible for Class A shares, whereas various parties hold Class B shares. The two largest owners of the B-class are Birta Pension Fund (37.44%) and Landsbankinn (22.89%). Owners of the B-class share capital have the right to attend general meetings, where they have full freedom of speech and priority to dividends from the company.

The value of the A-class of the foundation fund was 350 million króna at the end of 2021, and the value of the B-class of the foundation fund was 180 million króna. Over the last six months, the price of shares in the B-class of the foundation fund has ranged from 1.7 to 2.96, and their market value has therefore been between 306 and 532.8 million.

According to the SS membership register, there were 638 active contributors in 2021, whereas according to the society's 2021 annual accounts, there were 2,232 members with over 1,000 kr in the A-department's founding fund.

Regarding the influence of farmers on the management of the association, the arrangement is such that each branch (municipality) in the association's area appointed 1-5 representatives to the 2022 general meeting, with the number of representatives depending on the number of contributors in each area.

In the opinion of the Competition Authority, further investigation is required to establish whether farmers hold a clear majority stake in the association. Farmers also hold the voting power at general meetings, in accordance with the association's articles of association, which were adopted at the general meeting on 12 June 2020.

The Core Food of Norðlenska

The operations of Norðlenska, Kjarnafæði and SAH were merged in 2021 following a settlement between the companies and the Competition Authority. Following the decision of the Competition Authority, the companies' ownership was consolidated under the parent company, Kjarnafæði hf., and the company's name was changed to Kjarnafæði Norðlenska hf.

According to the information that formed the basis of the assessment of the merger, the combined company is minority-owned by farmers. Thus, the former owners of Kjarnafæði hold the majority, or a total of 54%, in addition to which Tani ehf. holds 1%, the company being owned by the former owners of Kjarnafæði. Furthermore, the former owner of Norðlenska, Búsæld ehf., holds a 43.1% stake in the combined company, with Búsæld being owned by farmers.

However, based on the information available at the time of the merger investigation, Búsæld was granted certain minority protection, which means that major decisions about the company cannot be made without regard to Búsæld.

Accordingly, Kjarnafæði Norðlenska is a minority-owned company, with the majority of its shares held by farmers. However, it does enjoy certain minority protection when making major decisions at the company level. The fact that the company is minority-owned by farmers means, among other things, that any potential distributions from the company flow, in part, to the farmers.

Slaughterhouse Society of the Vopnafjörður People

The Sláturfélag Vopnfirðinga operates a slaughterhouse in Vopnafjörður, where sheep and cattle are slaughtered.

KN holds a 34.81% stake in Sláturfélag Vopnfirðinga hf., Vopnafjarðahreppur holds a 25.61% stake, and the processing plant is minority-owned by farmers, while Búnaðarfélag Vopnafjarðar holds an 18.02% stake in the company. In the opinion of the Competition Authority, further investigation is required to determine whether farmers hold a clear majority of the voting power.

Under the conditions of the settlement between the Competition Authority and the merging parties regarding the merger of Kjarnafæði and Norðlenska, dated 12 April 2021, the merged company is required to continue certain transactions with the slaughterhouse. Furthermore, the combined company is required to offer farmers and their owned companies the opportunity to purchase the company's shareholding in the slaughterhouse. However, according to information in the slaughterhouse's 2021 annual report, KN's shareholding in the Slaughterhouse of Vopnafjörður has not changed.

Slaughterhouse of the West Húnvetninga Cooperative (SKVH)

KVH Slaughterhouse was established in 2006 and operates a slaughterhouse in Hvammstangi.

According to information from the Kaupfélag Vestur Húnvetninga (KVH) from 2021, farmers own a total of 41% of the cooperative. The abattoir is owned half by KS, which is discussed above, and half by the cooperative. KS therefore appears to exercise joint control of the company for the purposes of competition law.

At the end of 2021, KVH had 368 members in 6 branches. In accordance with the provisions of the Co-operative Societies Act, all members have equal voting rights at a general meeting. The exact proportion of KVH's members who are involved in farming is not known, but based on the above, the farmers' share of ownership in the company is not under their control. Available information suggests that the abattoir is a minority-owned farm.

B. Jensen

B. Jensen runs a slaughterhouse in Akureyri, slaughtering cattle and pigs. The company is owned by three non-farmers.

Fjallalamb Ltd.

The company operates a slaughterhouse and meat processing plant in Kópasker, but due to operational difficulties, its board decided to sell all of its autumn slaughter to another processing plant in 2022.

Fjallalamb was in minority ownership of farmers at the end of 2021. The company's largest owners were Seljalax hf. (21.31%), Byggðastofnun (21.21%), Norðurþing (15.31%) and the Agricultural Association of North-East Iceland (12.71%). The competitors SAH Afurðir (3.91%) and SS (0.81%) also hold a stake in the company. In the opinion of the Competition Authority, further investigation is needed to determine whether farmers hold a clear majority of the voting power.

Star-dust

Stjörnugrís hf. operates a pig farm and a meat processing plant and is owned by a family that has run the company for many years. Geir Gunnar Geirsson is the largest shareholder, holding half of the company's share capital. Other family members also hold shares. Based on the information available, the company is majority-owned by producers/farmers.

Kinglet

Ísfugl Ltd. operates a poultry farm, and carries out the slaughter and processing of poultry meat. The company is owned by Reykjabúið Ltd., which in turn is owned by Jón Magnús Jónsson, a poultry farmer. Based on the information available, the company is wholly owned by the producer/farmer.

Game bird

Matfugl ehf. specialises in the production of food products from poultry and pork, and is owned by the investment company Langasjávar ehf. Based on the information available, the company is majority-owned by producers/farmers.

6.2. Farmers' negotiating position weak – importance of competitive restraint – results of opinion polls

As noted above, the proposals in the draft bill appear to be based on the fundamental assumption that the interests of farmers and meat processing plants are entirely aligned. This is also the view of most who advocate for these changes. In this light, it is interesting to examine the views of farmers themselves regarding their own position, including in relation to meat processing plants.

As part of the investigation into the merger of Norðlenska, Kjarnafæði and SAH, the Competition Authority conducted two surveys of farmers. The first survey was aimed at gathering views for use in assessing the effects of the merger, while the second focused on gathering views on the conditions proposed by the merging parties to address the competition authority's preliminary assessment.

The first survey was sent to 3,843 email addresses and responses were received from 874 farmers who farm sheep, cattle, pigs or horses for human consumption. The responses were distributed as follows: 57% were sheep farmers, 34% were cattle farmers and 7% were horse farmers, while farmers whose main occupation was in another type of farming were a negligible minority.

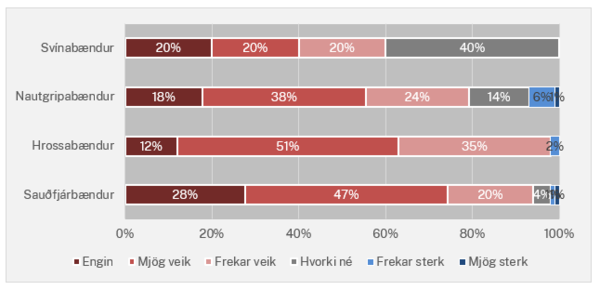

In the survey, farmers were asked, among other things, how strong or weak their bargaining position was in general vis-à-vis processing plants with regard to product prices and other terms. They considered 90% farmers their negotiating position vis-à-vis processing plants is weak or non-existent. Thus, just over 22% They have no negotiating position, hardly 45% they considered her to be very ill and bedridden 22% that she was rather ill. Horse and sheep farmers considered their situation to be the worst. See the farmers' positions by type of produce in the accompanying image.

When farmers were asked about their contractual position with the processing plant to which they had delivered the most animals, the majority considered their position to be weak or non-existent, or barely so. 82% farmers.

Farmers who are shareholders or members of a meat processing plant were then asked about their influence on their meat processing plant's policy. About 751 TP3T respondents felt they had little or very little influence. of its product station's policy.

Farmers were also asked why they considered their negotiating position to be weak vis-à-vis the meat processing plant. 475 written responses to the question were received. A thematic analysis of the responses revealed that 45% The respondents stated that they had no opportunity to influence prices or other decisions and that their views are not listened to. About 16% in addition, mentioned Problems related to the strong position of the processing plant towards farmers and limited options to look elsewhere.

Furthermore, farmers' attitudes towards the effectiveness of competition between meat processing plants were asked about in more detail.approximately 47% farmers had experienced problems due to a lack of competition between meat processing plants. Around 571 sheep farmers believed they had experienced competitive problems in this regard. Of those who had experienced competitive problems, mentioned 44% consultation between processing plants, oligopoly, lack of competition or monopoly.

The results of the survey also showed that regarding 30-50% The respondent had delivered livestock to more than one processing plant in the last 5 years, varying by product type. This is an indication that a considerable proportion of farmers are taking advantage of different options.

The survey also indicated that a significant number of farmers were interested in having more control over their produce. The following can be mentioned in this regard:

From the foregoing, it is unequivocally possible to draw at least two conclusions:

The explanatory memorandum to the draft bill specifically cites the difficult situation of meat processing plants as the reason for the planned exemption from competition law. One of the aims of the changes is said to be to support necessary restructuring, and that if no action is taken, the need for a shake-up is likely to increase further, with unforeseen demographic and social consequences. Letters from interest groups to the Icelandic government also call for exemptions where processing plants are at a disadvantage.

The memorandum accompanying the draft bill lists 19 slaughterhouse operators who would fall under the proposed exemption. The memorandum does not contain any comprehensive discussion of the financial position of these companies, but merely refers to the difficulties of individual companies in previous years and to recent analyses which, however, do not provide a detailed examination of the financial position of existing slaughterhouse operators.

For this reason, the Competition Authority requested all data held by the ministry on the financial position of the aforementioned slaughterhouse operators. In its responses, the ministry refers to a KPMG review of production facilities from June 2018 and a Deloitte analysis from April 2021, while for all other matters, it refers to the companies' annual accounts. The Ministry has therefore not obtained any data from the slaughterhouse licensees in connection with the preparation of the draft bill, beyond that which was previously obtained.

In preparing this review, the Competition Authority has therefore reviewed the analyses by KPMG and Deloitte, and has also conducted its own analysis based on information from the 2021 annual accounts.

It is worth pointing out, however, that these analyses are of varying scope:

In summary, these analyses show that the financial situation of some slaughterhouse operators is difficult, while the position of others is sound. The position of two of the three largest meat processing plants for sheep and cattle, namely KS and SS, is considered sound. The position of Kjarnafæði Norðlenska (KN) is weaker, but it has only been a short time since the merger of Kjarnafæði, Norðlenska and SAH. In KN's 2021 annual report, it is stated that due to the merger of the companies, cost-saving measures, access to loan facilities and a planned restructuring of the group's financing, management considers „that the group's going concern is assured for the foreseeable future.“ So, Stjörnugrís's position is very secure.

As for the smaller production plants, their EBITDA margin is positive on average; however, when depreciation and financing costs are taken into account, their performance is not strong, as their profit margin (profit/revenue) is negative on average. However, it should be noted that many of the smaller production plants where performance is poor are part of a group whose operations are robust.

From the above, it can be unequivocally concluded that the financial situation of meat processing plants in no way calls for exemptions from the law beyond other sectors of the economy, where the operating conditions of many companies are also difficult.

It should be noted in this regard that, in the application of competition law, a difficult financial situation or opportunities for efficiency gains may be taken into account when assessing the cooperation or mergers of undertakings.

7.1. KPMG report for the Ministry of Industry and Innovation, June 2018

In a KPMG report from June 2018, Assessment of production facilities, the purpose of the review was to „To analyse the costs of slaughtering, selling and distributing sheep products in order to identify ways that could lead to a reduction in slaughter costs and increased efficiency in the sector, for the benefit of farmers and consumers.“ The report deals exclusively with activities related to sheep farming.

Part of the report discusses the financial position and operation of product processing plants in the part of the sheep meat value chain that was examined in the report. The main findings of the report regarding this aspect are as follows:

7.2. Deloitte report for the Ministry of Industry and Innovation, 15 February 2021

In a Deloitte report from February 2021, the firm conducted a financial analysis of the position and opportunities for operational optimisation of domestic slaughterhouse operators in the slaughter and meat processing of cattle and sheep, at the request of the Ministry of Economic Affairs- and Innovation Ministry.

Part of the report is an analysis of the financial position and operations of slaughterhouse operators in the slaughter and meat processing of cattle and sheep. However, it is noted that the analysis is not a detailed analysis of the operations of the slaughterhouse operators, nor a validation of the data provided by them for the work. The analysis of operations led to the following main conclusions, subject to the above reservations:

8.3. The Competition Authority's analysis in December 2022

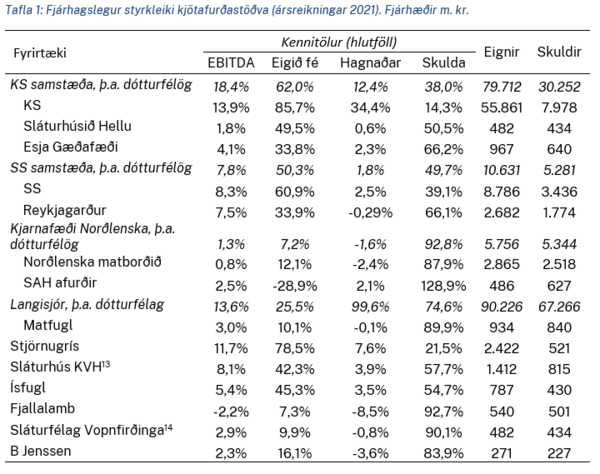

In connection with this review, the Competition Authority has analysed the financial position of the processing plants covered by the draft bill, based on information from the plants' 2021 annual accounts. It should be noted that in some cases, the processing plants are part of companies that engage in more diverse activities. Therefore, the results do not reflect the core operations of the processing plants, but rather provide important information about the economic position of their owners. For this reason, comparisons between the companies are subject to various difficulties.

Table 1 provides an overview of the key figures, assets and liabilities of the companies operating meat processing and product facilities, with data sourced from the companies' 2021 annual accounts. The table provides an overview of the key figures for the main processing plants, and their respective owners.

As can be seen from the table, SS and KS have a much stronger financial position than the smaller companies. KS's financial strength is significant, but looking at the equity ratio, it is around 621% for the KS group and around 861% for the parent company. This also applies to the so-called EBITDA margin.

As for the operation of Kjarnafæði Norðlenska, it was heavy in 2021, but it must be borne in mind that the merger of Kjarnafæði, The merger of Norðlenska and SAH took place in that year, and it is therefore likely that the costs associated with it had a negative impact on the combined company's performance during the year, and the anticipated benefits largely failed to materialise. It is therefore likely that the company's financial position, and consequently its competitive position, will improve in the coming years. This is in fact confirmed in the annual report, which states the following: „Due to the merger of the companies, cost-saving measures, access to credit lines and the anticipated restructuring of the group's financing, management considers the group's going concern to be secure for the foreseeable future.“

Operating margin, measured by EBITDA margin, is positive on average for the smaller production plants, but when depreciation and financing costs are taken into account, their performance is not strong, as their profit margin (profit/revenue) is on average negative. However, it should be noted that many of the smaller processing plants where operations are performing poorly are part of a group whose overall operations are sound. These include the Sláturhúsið á Hellu and Esju, which are owned by KS, as well as the Sláturhúss KVH, which is 50.1% owned by KS and 50.1% owned by Kaupfélag Vestur Húnvetninga. Furthermore, the operations of the poultry producer Ísfugl are on a good footing, and the operations of Stjörnugrís are very robust, with an EBITDA margin of 11.81% and a equity ratio of 78.51%.

Finally, it is worth emphasising that three corporate groups operate the majority of the country's processing plants, namely KS, SS and Kjarnafæði Norðlenska. Kaupfélag Skagfirðinga owns a 50.1% stake in Sláturhúsið KVH, but the company fully owns Esja Gæðafæði and Sláturhúsið Hellu. Kjarnafæði Norðlenska also owns a 35.1% stake in the Vopnafjörður slaughterhouse. Sláturfélag Suðurlands owns and operates its own meat processing plants. Despite the weaker financial position of the smaller companies, as outlined above, many of them are part of a financially strong corporate group. The companies are therefore part of a value chain that delivers a satisfactory rate of return.